When comparing Fidelity, Vanguard, and Schwab for IRA providers, it really depends on what you're looking for. If you want low-cost options, both Fidelity and Vanguard shine, with Fidelity offering zero expense ratio funds. For flexibility and accessibility, Schwab's user-friendly platform stands out, attracting active traders and those needing advisory services. Vanguard caters more to experienced investors focused on long-term growth with its index funds, while all three provide commission-free trading of individual equities. Each has its strengths, so consider your investment style and preferences to choose the best fit for your retirement goals. There's more to uncover about each provider's offerings.

Key Takeaways

- Cost Efficiency: Fidelity offers zero expense ratio funds, while Vanguard and Schwab have low expense ratios, enhancing long-term investment growth.

- Commission-Free Trading: Fidelity and Schwab provide commission-free trading for individual equities, while Vanguard charges a fee for options trading.

- Accessibility: Fidelity and Schwab have no account minimums, making them suitable for beginner investors compared to Vanguard's higher minimum investment requirement.

- Investment Options: All three providers offer diverse IRA account types, including traditional, Roth, and Gold IRAs, catering to various investor needs.

- User Experience: Fidelity's mobile app receives high ratings, while Schwab's mixed reviews and Vanguard's lower functionalities may impact user satisfaction.

2024 Apple MacBook Air with Apple M3 Chip (15-inch, 8GB RAM, 512GB SSD Storage) (QWERTY English) Midnight (Renewed)

- Processor: Apple M3 Chip with 8-core CPU

- Graphics: 10-core GPU for enhanced performance

- Design: Lightweight and under half an inch thin

As an affiliate, we earn on qualifying purchases.

Overview of Providers

When choosing an IRA provider, it's crucial to understand the strengths of each option available today. Vanguard is renowned for its low-fee investment products, particularly index funds and ETFs. However, keep in mind that some of its mutual funds require a minimum investment of $3,000 for IRAs.

If you're focused on cost-effectiveness, consider Fidelity, which offers a broad selection of commission-free mutual funds and ETFs, including options with zero expense ratios. This makes it particularly appealing for IRA investors looking to minimize costs. Additionally, many investors explore precious metals as an alternative investment strategy, with providers like Noble Gold specializing in Gold IRAs for retirement planning.

On the other hand, Charles Schwab provides a versatile range of investment choices, along with free robo-advisor services, catering to both passive and active investors.

Each of these providers—Vanguard, Fidelity, and Schwab—offers fee-free trading of individual equities within IRA accounts and various account types, such as traditional, Roth, and SEP IRAs.

While Vanguard is investor-owned and prioritizes cost reduction, Fidelity emphasizes customer engagement, and Schwab aims to balance shareholder profits with investor-friendly services. By understanding these nuances, you can better decide which provider aligns with your investment goals.

2023 Apple MacBook Air with Apple M2 Chip with 8-Core CPU/10-Core GPU (15-inch, 8GB RAM, 256GB SSD Storage) (QWERTY English) Midnight (Renewed)

- Display Size: 15-inch Liquid Retina display

- Build Material: Recycled aluminum enclosure

- Processor: Apple M2 with 8-core CPU

As an affiliate, we earn on qualifying purchases.

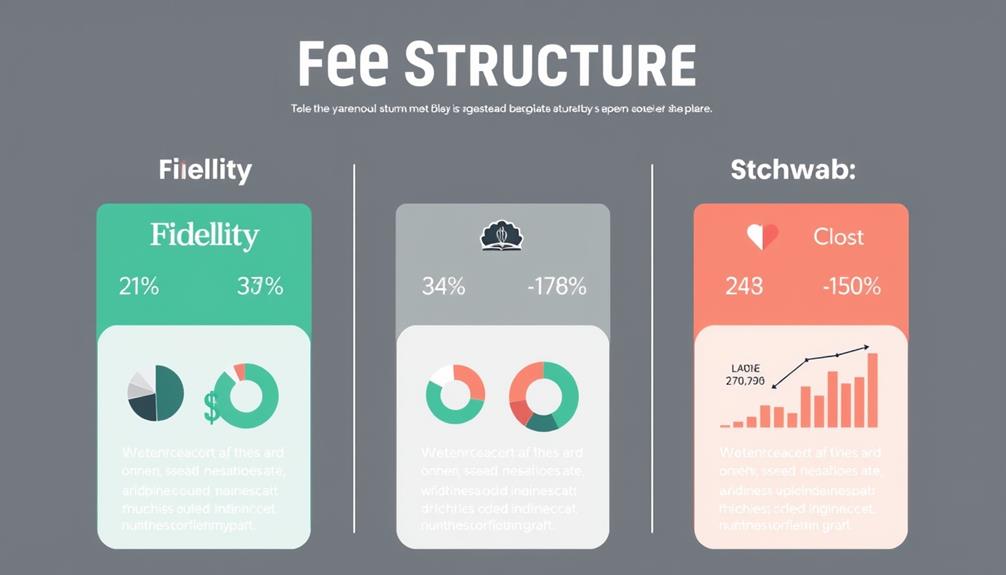

Fee Structures Comparison

When comparing IRA providers, you'll want to look closely at their fee structures, especially regarding commission-free trading options.

Understanding expense ratios can help you gauge the long-term costs of your investments, while margin trading rates may influence your trading strategy.

Additionally, considering the potential for higher returns with gold as a long-term investment can provide insight into how different providers may support your retirement goals through diverse investment options like converting 401k to Gold IRA.

Let's break down these key aspects to see which provider aligns best with your financial goals.

Commission-Free Trading Options

Understanding the fee structures of IRA providers can greatly impact your investment strategy. When it comes to commission-free trading, all three brokerages—Fidelity, Vanguard, and Schwab—offer attractive options for your individual retirement accounts (IRAs).

Fidelity and Schwab shine by not charging any commissions or trading fees for individual equities, giving you an edge in managing your investments without worrying about extra costs. This is especially beneficial when considering the importance of budgeting and managing expenses effectively.

Vanguard, while also providing commission-free trading for stocks and ETFs, does charge a slight fee of $1 per contract for options. This is worth noting if you're considering options trading as part of your IRA strategy. Additionally, Fidelity distinguishes itself by offering numerous funds with no expense ratio, appealing to cost-conscious investors looking to maximize their returns.

Both Fidelity and Schwab maintain no trade or account minimums, making them accessible for all investors. When it comes to options trading, Schwab and Fidelity offer low transaction costs at $0.65 per contract, compared to Vanguard's $1 fee. This competitive pricing can considerably enhance your investment experience, allowing you to focus on growing your retirement savings.

Expense Ratios Overview

Choosing an IRA provider can feel overwhelming, but focusing on expense ratios can simplify your decision. Understanding these fees is essential, as they directly impact your long-term returns. Here's a quick comparison of the expense ratios for Fidelity, Vanguard, and Schwab:

| Provider | Expense Ratio Start |

|---|---|

| Fidelity | 0.00% (zero funds) |

| Schwab | 0.02% (ETFs) |

| Vanguard | 0.03% (ETFs) |

Fidelity truly stands out with its zero expense ratio funds, making it an appealing choice for cost-conscious investors looking to minimize fees within their IRA accounts. Schwab follows closely, offering ETFs with expense ratios as low as 0.02%, perfect for those who prioritize low-cost investing. Vanguard also emphasizes affordability, with expense ratios starting at 0.03%, though keep in mind its minimum investment requirements for some mutual funds.

All three providers focus on passing savings onto investors, allowing your IRA investments to grow more effectively over time. Remember, the lower your expense ratios, the more you can potentially accumulate in your retirement account!

Margin Trading Rates

Margin trading can be a powerful tool for investors, but knowing the associated rates and fee structures is essential for making informed decisions. When evaluating IRA providers, you'll find notable differences in margin trading interest rates.

Fidelity stands out with the most competitive rate at 4% for high-net-worth clients, making it an appealing choice for those looking to minimize borrowing costs. Understanding common financial terms is vital when maneuvering these options.

Vanguard follows closely with a margin trading interest rate of 4.75% for clients boasting a million-dollar net worth. However, Schwab's rates are considerably higher, ranging from 8.3% to 8.5%, which can greatly impact your overall investment returns.

In addition to interest rates, consider the cash management practices of each provider. Vanguard incentivizes you by paying for uninvested cash at approximately 0.7%, while Schwab and Fidelity retain most earnings from uninvested cash.

This difference can further influence your net returns, especially if you hold a substantial cash balance within your IRA. By carefully analyzing margin trading rates and cash management strategies, you can make a more informed decision about which IRA provider aligns best with your investment goals.

2023 Apple MacBook Air with Apple M2 Chip with 8-Core CPU/10-Core GPU (15-inch, 16GB RAM, 1TB SSD Storage) (QWERTY English) Midnight (Renewed Premium)

- Processor: Apple M2 8-Core Chip

- Memory: 16GB Unified RAM

- Storage: 1TB SSD

As an affiliate, we earn on qualifying purchases.

Services and Features Offered

When choosing an IRA provider, you'll want to contemplate the variety of investment account types available, as well as the advisory services each firm offers.

Some providers excel in educational resources, helping you make informed decisions for your retirement savings.

Additionally, it's important to be aware of potential investment risks like avoiding gold IRA scams and understanding how to manage volatility in your assets.

Let's explore how Vanguard, Fidelity, and Schwab stack up in these key areas.

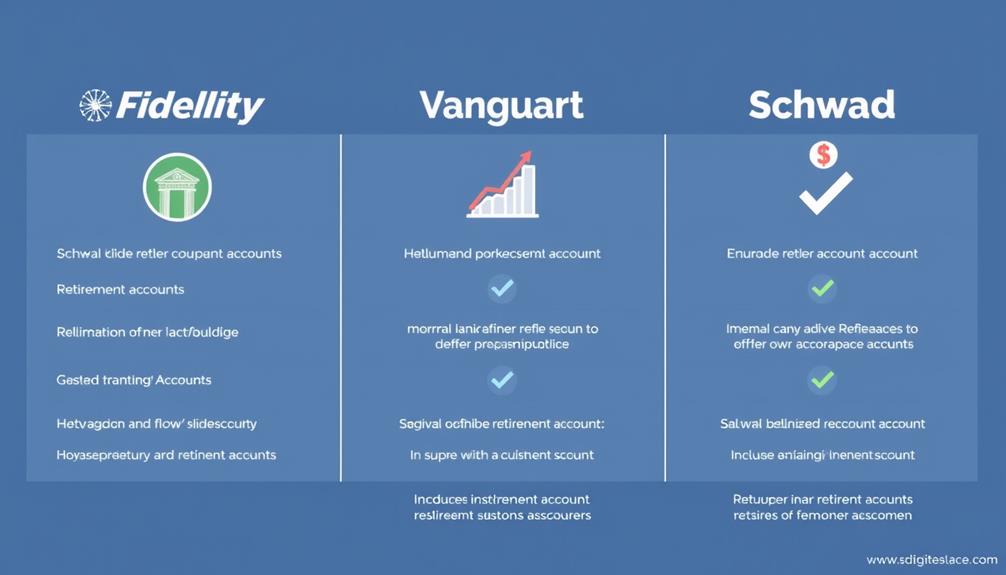

Investment Account Types

Investors can explore a range of IRA account types offered by leading brokerage firms like Fidelity, Vanguard, and Schwab, each designed to meet various retirement savings goals.

You'll find traditional IRAs, Roth IRAs, and SEP IRAs among the investment account types available. Additionally, for those looking to expand their retirement portfolio with alternative assets, options like Gold IRAs can provide a valuable hedge against economic uncertainties and inflation, offering unique tax advantages and long-term growth potential through Gold IRAs' benefits.

- No account minimums at Fidelity and Schwab, making it easier to start saving.

- Fee-free trading of individual equities within IRA accounts, letting you invest without extra costs.

- Robust educational resources and planning tools to enhance your investment decisions.

While Vanguard typically requires a $3,000 minimum for certain mutual funds, Fidelity and Schwab excel in providing accessible options.

They also offer lower or no minimum balances for their robo-advisor services. This flexibility is essential for investors looking to maximize their retirement savings with different investment styles.

Additionally, both Fidelity and Schwab emphasize customer service, ensuring you have the support you need while managing your individual retirement accounts (IRAs).

Advisory Services Offered

Advisory services play an essential role in helping you navigate your retirement investment options effectively. Vanguard offers a more traditional approach to advisory services, requiring a minimum investment of $50,000. This service focuses on low-cost index and mutual funds, making it ideal for long-term investors who value a hands-off strategy.

In addition, investing in precious metals, like gold, can provide a valuable diversification benefit for your retirement portfolio, protecting against market volatility and inflation risks gold investment strategies.

On the other hand, Fidelity Go provides a light advisory service with no minimum balance, allowing you to access professional management without a significant upfront investment. This flexibility gives you the freedom to start investing at your own pace.

Schwab takes a modern approach with its Schwab Intelligent Portfolios, a robo-advisor that customizes investment strategies based on your preferences. This service comes with no advisory fees and a low minimum investment, making it accessible for more investors.

All three firms enhance their appeal by offering various account types, including individual retirement accounts (IRAs) and taxable investment accounts.

They also integrate financial planning tools and educational resources, helping you make informed decisions and optimize your IRA contributions. With these advisory services, you can choose the level of support that best fits your investment style and retirement goals.

Educational Resources Available

Steering through your IRA options can be overwhelming, but having access to extensive educational resources can make a significant difference. Whether you're just starting out or looking to refine your investment strategies, Fidelity, Vanguard, and Schwab all offer valuable tools to help you navigate your choices.

By focusing on content quality, these platforms guarantee that the information is credible and trustworthy, enhancing your learning experience.

- Fidelity provides a user-friendly learning center with interactive tools for all levels of investors.

- Vanguard emphasizes long-term investing with resources focused on low-cost index funds and portfolio diversification.

- Schwab offers a robust mix of educational materials, including personalized investment guidance through its robo-advisor services.

Each platform integrates these educational resources directly within their trading interfaces, making it easy for you to learn while you manage your investments.

With articles, videos, and webinars at your fingertips, you can confidently explore your IRA options and develop effective investment strategies.

2025 Apple MacBook Air with Apple M4 Chip (15-inch, 16GB RAM, 256GB SSD Storage) (QWERTY English) Silver (Renewed)

- Lightweight and Portable: Blaze through work and play anywhere

- Powered by M4 Chip: Enhanced speed and fluidity for multitasking

- Up to 18 Hours Battery Life: Long-lasting battery for all-day use

As an affiliate, we earn on qualifying purchases.

User Experience and Accessibility

Steering your investment options can be a breeze with the right tools, and the user experience offered by IRA providers plays an essential role in this process. Fidelity stands out with its highly rated mobile app, boasting 4.8 stars on Apple and 4.5 stars on Google Play, making account management and trading user-friendly. On the other hand, Schwab's app shows mixed results, achieving 4.8 stars on Apple but only 2.2 stars on Google Play, indicating a less consistent experience. Vanguard's mobile app has improved, earning a 3.5-star rating on Google Play and 4.7 stars on Apple, showcasing better reception among iOS users.

Here's a quick comparison of the mobile apps:

| Provider | Apple Rating | Google Play Rating |

|---|---|---|

| Fidelity | 4.8 | 4.5 |

| Schwab | 4.8 | 2.2 |

| Vanguard | 4.7 | 3.5 |

All three platforms provide robust online experiences for managing your brokerage account, but Fidelity and Schwab offer specialized tools for active traders. Vanguard may lag in this area, potentially affecting user experience for those seeking advanced functionalities.

Target Investor Types

Choosing the right IRA provider goes beyond user experience; it's also about finding the one that aligns with your investment style. Each provider caters to different target investor types, ensuring you have options that suit your needs. For those considering alternative investments, such as precious metals, understanding the benefits of a Gold IRA rollover can enhance your retirement security and diversify your portfolio Gold IRA Rollovers.

- If you're an experienced investor looking for low-cost index and mutual funds, Vanguard is your best bet, requiring a minimum investment of $3,000 for select funds.

- For beginners or active investors seeking a wealth of educational resources and commission-free trading, Fidelity stands out with its extensive products and services.

- If you thrive on active trading and appreciate user-friendly platforms along with personalized advisory services, Schwab has you covered, boasting around 400 branches nationwide.

All three firms facilitate fee-free trading of individual equities, making them accessible to a broad spectrum of investors.

Whether you're just starting to explore individual retirement accounts (IRAs) or you're a seasoned pro aiming to optimize your portfolio, these providers have tailored offerings that can help you reach your financial goals.

Key Takeaways and Recommendations

When it comes to selecting the right IRA provider, understanding the key differences among your options can make all the difference in your investment journey.

If you're looking for flexibility and a wide selection of commission-free funds, Fidelity is an excellent choice. With no account minimums, it's perfect for those just starting or wanting to explore various individual retirement accounts (IRAs) without heavy initial investment.

Additionally, many new investors may find value in exploring best websites to earn money online to supplement their income as they build their retirement savings.

On the other hand, if you're a long-term investor focused on low-cost index funds, Vanguard might suit your needs better, despite its higher minimum investment requirements.

However, if you value a balance of services and a user-friendly trading platform, Schwab could be your best bet. It offers no account minimums and appeals to both active traders and those seeking advisory services.

For those who want to avoid high thresholds for advisory services, both Fidelity and Schwab provide accessible options.

Ultimately, your choice should align with your investment preferences, whether that's flexibility, low costs, or a combination of personalized services.

Choose wisely, and you'll set the stage for a successful investment journey.

Frequently Asked Questions

Who's Better, Charles Schwab or Fidelity?

Choosing between Charles Schwab and Fidelity depends on your needs. If you value extensive research and a user-friendly app, Fidelity's your pick. However, if you want personalized services and low ETF expenses, Schwab's the better choice.

Who Performs Better Fidelity or Vanguard?

Imagine two skilled gardeners—Fidelity and Vanguard. When you compare their yields, you'll find Fidelity's garden flourishes with diverse, low-cost options, while Vanguard's blooms beautifully but often requires more care. Choose based on your investment style.

What Is the Best Company to Open an IRA With?

When you're looking to open an IRA, consider factors like fees, investment options, and account minimums. Choose a company that aligns with your financial goals and offers the features that best support your investment strategy.

Is Fidelity the Best for IRA?

If you're considering Fidelity for your IRA, you'll appreciate its commission-free funds, no minimum balance requirements, and excellent educational resources. These features make it a strong contender for your retirement investment needs.

Conclusion

In the battle of IRA providers, Fidelity, Vanguard, and Schwab each bring unique strengths to the table. Depending on your investing style and needs, one may suit you better than the others. Don't let the decision feel like trying to use a rotary phone in a smartphone world; consider fees, services, and user experience before choosing. Ultimately, take the time to assess what matters most to you, and you'll find the right fit for your financial future.